{kind=link}

🏚️ A Record-Breaking Red Flag

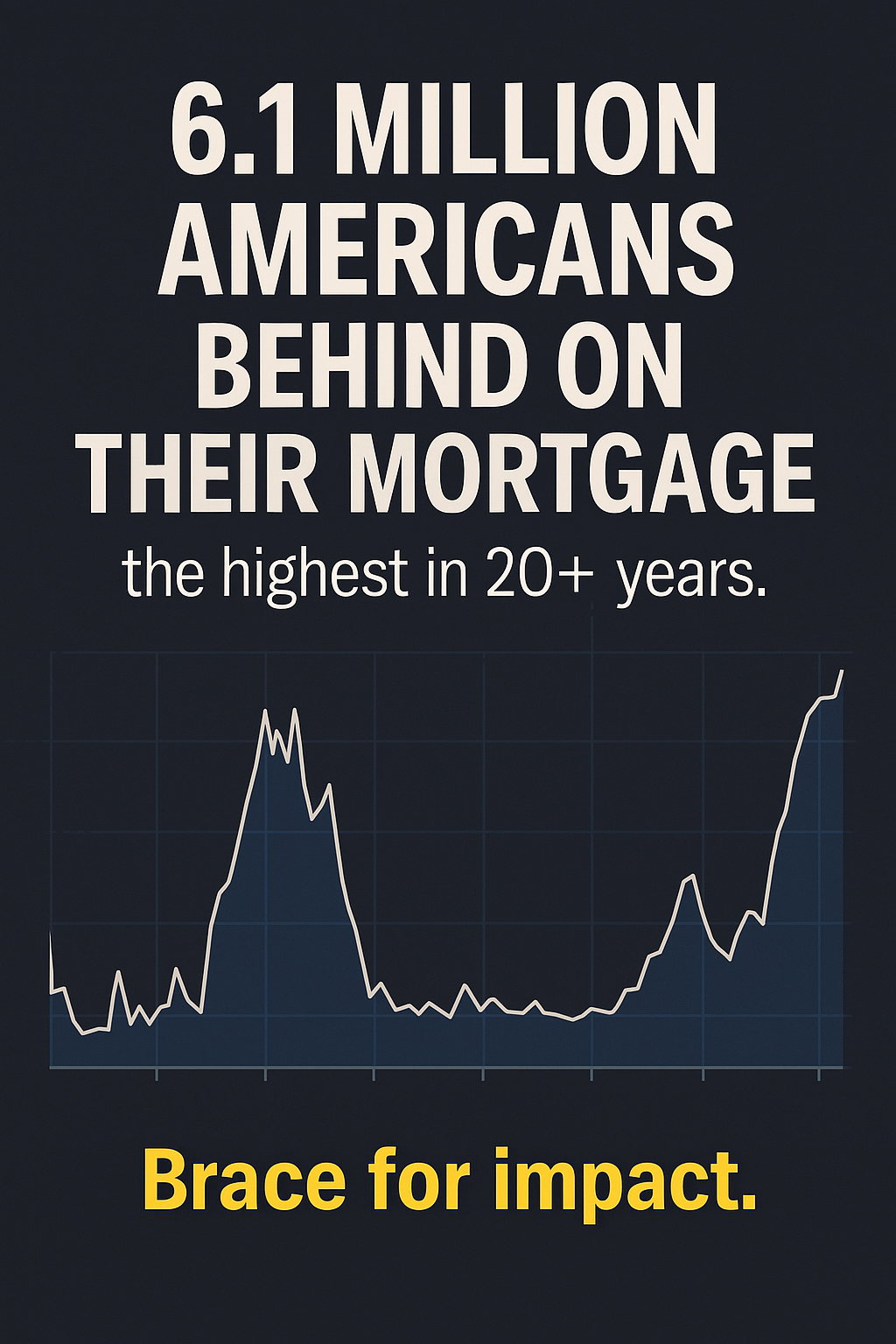

Brace yourselves — the numbers are in, and they’re alarming. Entrepreneur and media personality Patrick Bet-David recently sounded the alarm on Facebook, revealing that over 6.1 million Americans are currently behind on their mortgage payments — the highest level in more than two decades.

A Bloomberg screenshot shared in his post shows Freddie Mac’s serious delinquency rate hitting 0.42% as of January 31, 2025 — a level we haven’t seen since the fallout of the 2008 subprime mortgage crisis.

“Brace for impact,” Bet-David warns — and rightfully so.

This isn’t just a blip on the radar. It’s a signal that financial turbulence is back — and this time, the world is watching with very different tools and options in hand.

🏦 What’s Happening to the Traditional Financial System?

The American dream is cracking. Rising interest rates, unaffordable housing prices, wage stagnation, and inflation have created the perfect storm. Millions of people, especially those who bought during the pandemic housing boom, are now struggling to keep their heads above water.

If this trend worsens, we could be looking at:

- A new wave of foreclosures

- Regional banks under pressure (again)

- A slowdown in consumer spending

- Recession fears returning full force

But here’s the twist: this time, the world has an alternative.

💥 Enter: Crypto Finance

When the 2008 financial crisis hit, people had no choice but to watch institutions fail, bailouts flood the system, and banks walk away unpunished. That disaster gave birth to Bitcoin — literally. The first Bitcoin block in 2009 contained the message:

“Chancellor on brink of second bailout for banks.”

Now in 2025, crypto isn’t just a fringe movement — it’s a growing parallel financial ecosystem. Here’s why this mortgage crisis could be a turning point for decentralized finance:

🔄 1. Crisis Breeds Innovation

History shows us: economic crises fuel paradigm shifts. In 2008, we got Bitcoin. In 2020, DeFi exploded. In 2025, we might just see:

- A surge in crypto adoption by the mainstream

- More people turning to self-custody wallets

- Interest in stablecoins over traditional savings

- The rise of on-chain lending and borrowing as alternatives to failing institutions

🪙 2. Bitcoin = Digital Gold in Times of Fear

In moments of uncertainty, people seek stores of value. Bitcoin has increasingly played the role of digital gold — a scarce, non-sovereign asset immune to money printing and political games.

If trust in banks continues to erode, we expect a capital shift into Bitcoin and Ethereum, not just from retail investors but potentially even from small institutions and hedge funds looking for hedges against fiat instability.

📈 3. DeFi > TradFi for the Next Generation

The younger generation has grown up during endless financial crises, scandals, and inflation. They’re not loyal to banks — they’re loyal to functionality. If DeFi gives them faster access to credit, global remittances, and yield opportunities — why go back?

In fact, we’re already seeing:

- More users onboard via Web3 wallets

- Increased usage of decentralized stablecoins like DAI

- Rising interest in real-world assets tokenized on-chain

🧿 TheCoincierge’s Take

This is more than a mortgage crisis. It’s another signal that traditional systems are outdated, fragile, and inaccessible to many.

Crypto isn’t just surviving — it’s positioned to thrive when the old system cracks. We’re not saying a financial collapse is good news — far from it. But it’s in moments like this that the world starts looking for better alternatives.

And this time, we have them.

So yes — brace for impact, but also…

prepare for opportunity.

Stay weird. Stay awake.

🧿 TheCoincierge is watching.

Sources:

- Patrick Bet-David’s Facebook post

- Freddie Mac Delinquency Data (via Bloomberg Terminal)